Dr Pepper Snapple: Spin-off Bargain?

On Wednesday the 7th, Dr Pepper Snapple Group ($DPS) officially began to trade. Its $25 price tag is lower than many expected after the soft-drink maker was spun-off of its parent company, Cadbury Schweppes.

Because spin-offs in general beat the market (and can make for excellent hunting grounds), I'm always looking for potential purchases. DPS stands out because of its well recognized brand names, competitive advantage, and unique spin-off situation. Cadbury, its prior owner, trades on the London Stock Exchange. But when DPS was spun-off, it traded on the NYSE. This is a problem for mutual funds and institutions in the UK that owned Cadbury. They can't or don't want to hold a foreign-traded security. So more than likely (this may have already started), these institutions will sell their newly received DPS shares without regard to price. Some of the brands of DPS include: Dr Pepper, Snapple, 7 UP, Motts, Sunkist, A&W, Hawaiian Punch. This post isn't meant to be a complete analysis of the investment, just my initial thoughts on a potential opportunity.

Comparisons

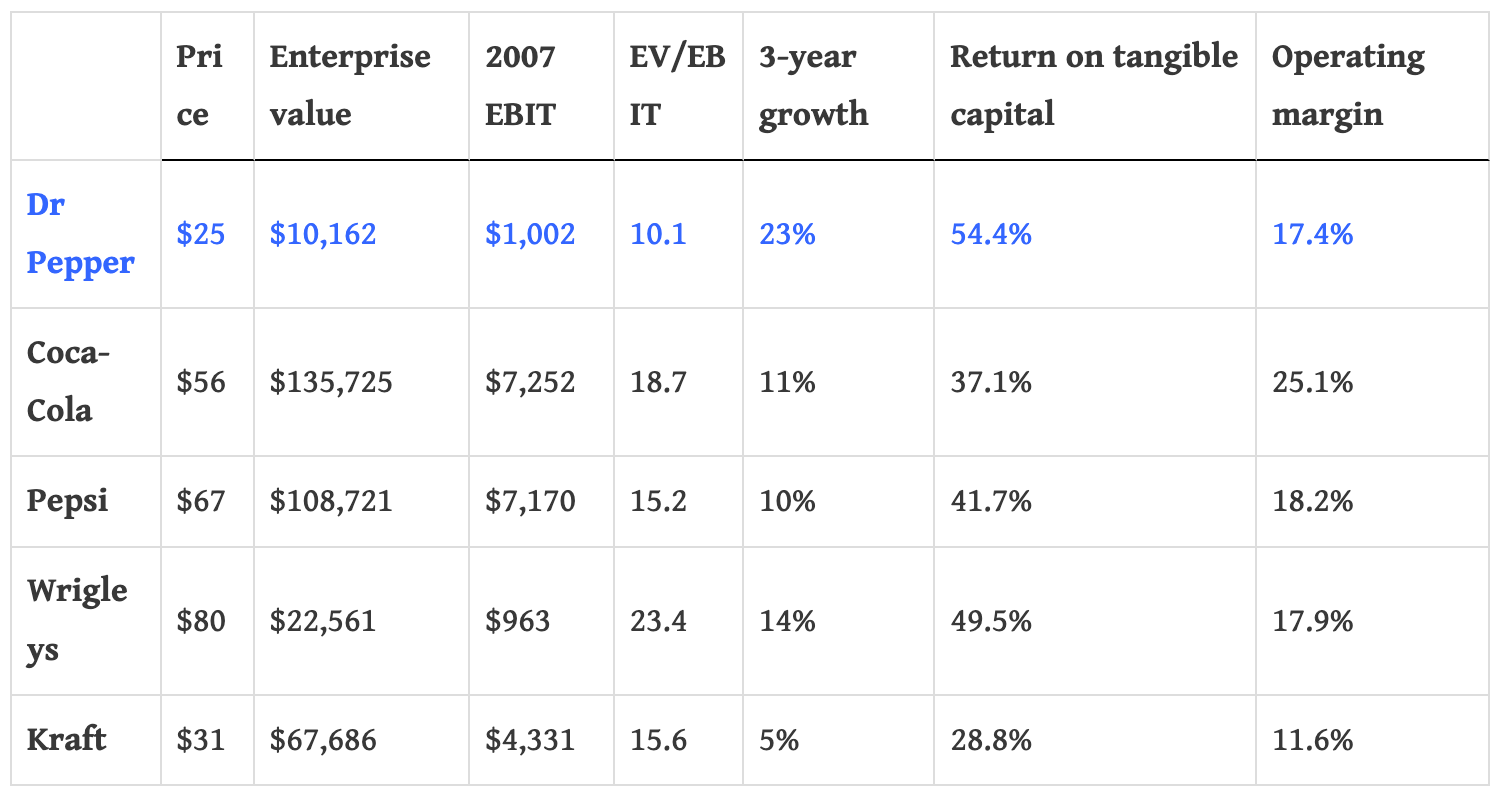

The table below compares DPS with other soft-drink and consumer goods companies.

As you can see from the above, DPS looks fairly cheap on a relative basis. Let's compare Dr Pepper's current price with the recent buyout of Wrigley's by Mars and Warren Buffett:

Dr Pepper earns about the same pre-tax amount as Wrigley's. Operating margins are approximately the same (17-18%), and Dr Pepper has a slightly higher ROIC. On a normalized basis, it looks like Dr Pepper's margins may be around 19-20% of sales. In the last three years, Wrigley grew sales 14% annually versus Dr Pepper's 23% (although DPS had declining margins).

So with the above comparisons, why did Buffett/Mars offer over twice as much for Wrigley's? Was it international growth? Strength of the brand name? More potential for gum/candy than Carbonated Soft Drinks(CSD)?

Reflections on Coca-Cola

In 1988 and 1989, Warren Buffett loaded up on shares of Coca-Cola at a split-adjusted price of $5.48. At the time, Coke had a EV/EBIT multiple of about 9-10x. Ten years later (1998), Coke had reinvested about $7.4B, and increased pre-tax income by $3.4B. This comes out to a 45% return on incremental capital invested. An extremely high return over a ten-year period for a company of Coke's size (thanks to the moat).

I don't want to make too many comparisons between Coca-Cola and Dr Pepper Group. They sell similar products, and have valuable brand names, but very different economics. Coke has huge international presence, and a much larger share of the CSD market. Management at Dr Pepper have targeted for high-single-digit income growth. To me, little international presence seems like more of an opportunity than anything else... Despite the differences, DPS may be a potential takeover target for a larger consumer goods company or even Mr. Buffett himself. Stay tuned for further research...

Disclosure: We do not own any security mentioned in this post.