Berkshire's Best Investments + Poster Now Available

[This is a cross post from the Explorist Productions blog. Explorist is a media company I founded that publishes content related to business, innovation, and discovery.]

The Berkshire Hathaway limited hardcover letters book and “50 Years of Berkshire” wall print are now available for purchase online. Both of these items were available at the meeting a month ago and I’ve received lots of praise about them from other shareholders, so I’m glad to finally make them available to everyone.

In the process of doing research for the visualization, I collected a lot of data on Berkshire's financial history -- much more data than could fit in the charts on the print.

So in addition to the wall print, I hope to release a few more posts further exploring the story of how Warren Buffett transformed Berkshire over the years. Once I reformat and clean-up it up, I’ll eventually release the raw data so that others can do their own analysis.

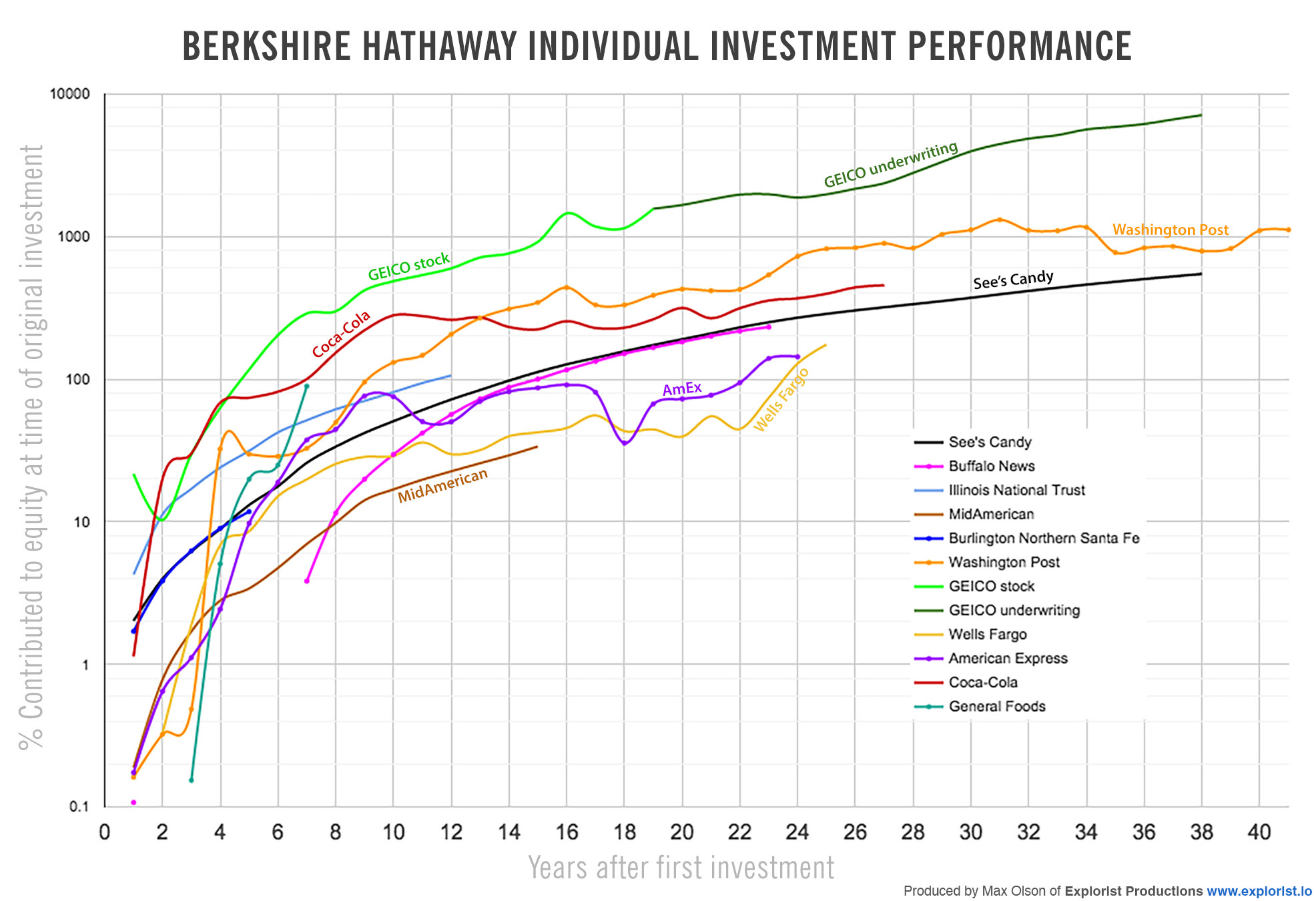

Berkshire Hathaway’s Best and Most Notable Investments

The following chart shows the cumulative contribution to book value* of selected investments over 50 years. This is a good yardstick for comparing how successful investments were over time. It doesn’t include insurance companies other than GEICO, as it’s too difficult to separate individual performance given available data.

Notes:

See’s Candy: Income for some years after 23 are estimated.

Buffalo News: No data available after year 23.

BNSF: Post-acquisition performance only (pre-2009 stock return not included).

Dividend income for stock holdings calculated in most cases on average shares held during year.

Some interesting tidbits:

One-third of Coca-Cola’s total gain to Berkshire is in dividends paid over the 27 year holding period. One-quarter of the Washington Post gains are from dividends, the remainder from realized gains in the 2014 sale/transfer.

With underwriting gains, GEICO has added 7,119% to book value since purchase in 1976. This means that had the rest of Berkshire’s investments returned 0% over those 38 years, annual book value growth would still have been 12%.

* A simple example to show the calculation: ABC Corp. is purchased in year 1, adding $100 (either in net income for subs, or change in unrealized gains + dividends for investments) that year to an initial equity base of $1,000. So contribution after year 1 would be 10%. In year 2, ABC Corp. adds another $100 to a starting equity base of $1,300. Contribution for that individual year would be 100/1300 = 7.7%, but cumulative contribution would be 20%, as ABC Corp. has contributed $200 to an initial equity base of $1,000.

This measurement puts investments on an equal footing, allowing comparison across different timeframes. It implicitly accounts for both individual return and capital allocated to the investment. What is not accounted for is excess capital reinvestment — in other words, contribution is based on GAAP net income, not true free cash flow.